What Is An Ica In Merchant Services

Have you e'er wondered what, exactly, a "merchant services provider" is? What does a merchant services provider practice, and how tin working with i do good your company?

Briefly put, a merchant services provider handles electronic customer payment transactions for merchants. By serving as an intermediary betwixt the merchant's and client'south banks, the merchant services provider is able to facilitate the transfer of customer funds to merchant accounts.

During the early on 1970s, people were getting weary of the paper-based system. The major problems were losses and huge overhead, non to mention that merchants had to wait up to two weeks for their money. There was a tremendous need for automation and a more price and fourth dimension constructive way to process transactions. To respond this demand, both card associations introduced electronic payment systems in 2 stages.

The "authorization" system was revamped in 1973. Potency is the process of guaranteeing there is adequate credit available on the card and capturing that authorized corporeality to reduce the available credit. This was previously based on a floor limit and a telephone telephone call was placed to a call centre for any corporeality over the floor limit. NBI introduced BASE 1 (Bank of America Organization Engineering science 1) which was their electronic online potency system. That aforementioned twelvemonth Master Charge introduced INAS (Interbank National Authorization System) for "online" authorizations.

In 1974, NBI introduced BASE 2 for online electronic clearing and settlement while Master Accuse introduced INET (Interbank Network for Electronic Transfer). Besides, in 1974, Banking company of America'south international licensees chartered an international company, IBANCO, to administrate BankAmericard, Inc., outside the U.S. Past the belatedly 1970s, the Interbank Card Clan (ICA) had members from equally far away every bit Africa and Australia. To reverberate the commitment to international growth, ICA changed its name to Mastercard. Although Visa and Mastercard are two distinct organizations, all banks today are members of both associations. It was not ever this way, only in the 1970s they realized that it was to everyone's benefit to work together.

By 1979, electronic processing was progressing. Dial-up terminals and magnetic stripes on the back of credit cards were introduced thus enabling retailers to swipe the client'south credit card through the electronic terminal. These terminals were able to access the issuing bank's cardholder information. This new technology gave authorizations and processed settlement agreements in a thing of 1 to two minutes. The reduction in paper was an added and much appreciated benefit.

In 2008, Discover joined the interchange model of doing business, and now most acquiring banks offering all major credit cards.

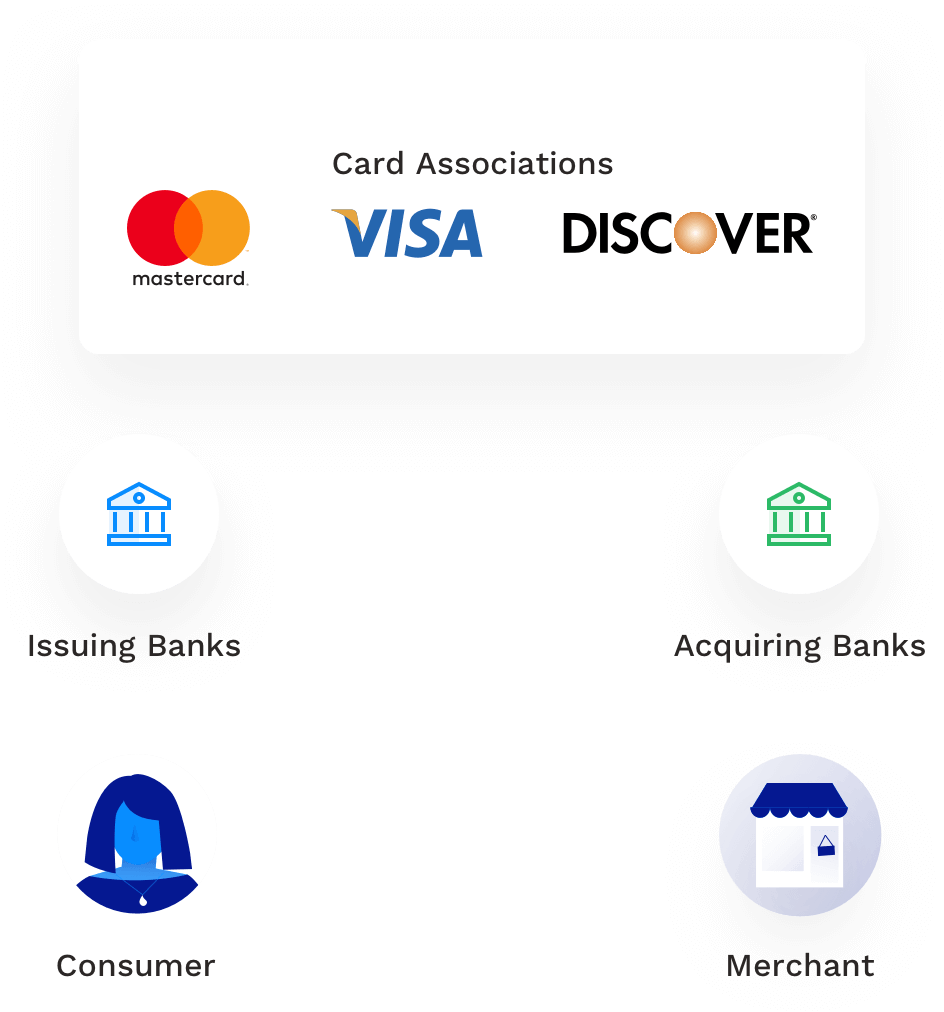

Footstep 3: The merchant bank captures the transaction and forwards the information to the customer's carte-issuing depository financial institution through the depository financial institution card clan network.

Footstep 4: The association organisation and so routes the transaction to the issuing banking company and requests an approving. The transaction is canonical or declined depending on the status of the cardholder'southward account.

Step 5: The issuing bank sends dorsum the response. If the transaction is canonical, the issuing banking concern assigns and transmits the authorization code dorsum to the card clan.

Stride 6: The authorization code is sent from the card association to the acquiring depository financial institution.

Step 7: The acquiring banking company routes the approval lawmaking or response to the merchant's terminal. Depending on the merchant or transaction blazon, the merchant'south concluding may print a receipt for the client to sign (or the customer signs electronically), which obligates the client to pay the corporeality approved.

Step 8: The issuing bank bills the client.

Step 9: The customer pays the bill to the issuing banking company.

The disbelieve fee that a merchant is charged depends on several factors including the following:

Blazon of business (i.e. industry, brick-and-mortar or e-commerce, etc.)

The merchant'south industry type—such as fast food, colleges, warehouses, gas stations, and more—affects rates. Each transaction must meet one or many factors to authorize for a specific category. Some factors determine if the transaction will exist completed, while others determine the rate and transaction fee that will exist assessed.

A scattering of industries take been assigned a special rate category. In some cases, preferred rates were established to attract merchants to accept credit cards.These include warehouse clubs and supermarkets. In other cases, categorization rules reverberate the unique transaction menstruum for a detail industry; for example, lodging and motorcar rental businesses crave authorization at check-in days before a transaction is settled. This means that boosted data points similar inflow and checkout dates, folio numbers, and length of rental are required to be sent to Visa or Mastercard forth with the credit carte data. To authorize for these categories, merchants must use industry-specific software or concluding applications, which prompt for the extra information. They must also properly transmit it to Visa or Mastercard.

As a result of new technologies, such as Mobil Speed passes, rates accept been created for gas stations, fast food restaurants and convenience stores. Fast food and gas station transactions are normally completed without a signature and are considered more than secure than MOTO (post society telephone order) or Net transactions, mainly due to the limit attack the amount of each transaction.

Type of bill of fare processed (i.e., traditional credit cards, corporate, rewards based, purchasing or check cards)

Visa and Mastercard have created an endless list of names for virtually the same production. The deviation between the various commercial cards is divers past the reporting features available to the cardholder.

Commercial cards are designed to aid companies maintain control of purchases while reducing the administrative costs associated with authorizing, tracking, paying and reconciling those purchases.The interchange rate for commercial cards is unlike than the per transaction rate for the average consumer card. In most cases, the interchange cost is higher than the consumers' rate.

Bank check cards, offline debit or signature-based debit transactions are routed through the Visa/Mastercard authorization and settlement system. Transactions are settled nightly and authorized by the cardholder's signature. Due to the decreased run a risk factor, these transactions are at a lower charge per unit structure. Proceed in mind that the money is not loaned; it is coin that is already in ane's checking account.

Check card transactions fall into a number of categories. Visa and Mastercard established bank check card rates that are priced significantly lower than all other consumer credit cards. These new categories provide however some other style for processors to create unique rate offerings.

How a card is processed (i.e., card present or card non present, swiped, dipped, etc.)

Determining what a merchant will exist charged is based on the method of card entry and what information is entered. The first and most obvious factor is whether the card is physically present at the POS. Whenever a menu is swiped (magnetic stripe) or dipped (EMV scrap) through an electronic concluding or card reader, an indicator is transmitted to Visa or Mastercard, along with the balance of the information. It records the fact that the information was received directly from the card's magnetic stripe. Without this indicator, the transaction is not eligible for any swiped interchange category.

Magnetic stripe and EMV chip technology has been incorporated into more and more products. Readers tin be establish in computer keyboards, jail cell phones attachments, and more than. Whereas it is relatively easy to capture the information from a magnetic stripe or scrap, it is entirely unlike to properly transmit the information to Visa and Mastercard in a fashion that will let the transaction to authorize for a certain charge per unit.

It is possible and, in fact, common for merchants to believe they are qualifying for the all-time swiped/dipped rates, when in fact their transactions are downgrading, which means higher transaction fees for them. Merchants should exist encouraged to exam transactions and accept their processor verify their qualification levels instead of assuming that a swipe/dip will e'er qualify for a certain rate.

Note that Visa and Mastercard both make a distinction between a carte du jour that was cardinal entered due to a bad magnetic stripe equally opposed to a transaction where the cardholder is non present, such equally in MOTO or Internet orders. To avoid confusion, merchants should follow one simple rule to ensure that they qualify for either the cardinal entered or the card-not-present rate: Whenever a carte du jour is not swiped, enter the data required for Address Verification Service (AVS) every bit well as an "order number" for every transaction. The society number tin be any length.

Additionally, certain categories take strict qualifications, such as merchant category, merchant actions and transaction size. For most categories, the interchange cost is a combination of a percentage rate and a transaction fee.

- Risk presented

- Merchant credit

- Other Factors

Transaction qualification is influenced by many factors. In many cases, the only way to truly know how merchants can minimize interchange costs is to critically examine their bankcard statements.

Transactions are downgraded when they don't run into interchange requirements, such equally not capturing the correct bill of fare information at the POS; settling the transaction later on a deadline has lapsed; or key-entering rather than swiping/dipping a card. A downgraded transaction ways a higher cost for the merchant.

What Is An Ica In Merchant Services,

Source: https://www.fidelitypayment.com/resources/what-are-merchant-services/

Posted by: gonzalezwitepheres.blogspot.com

0 Response to "What Is An Ica In Merchant Services"

Post a Comment